Tinker, Tailor, Soldier, Spy

Tinker, Tailor, Soldier, Spy

Which is which in macro economic terms?

The macro winds of change appear to have arrived, while some market participants boil themselves on summer vacations, earning a well deserved break from this vicious and unexpected bull market for equities, others toil away. Could we be hitting the limit of monetary policy tools? Or will consumer spending continue unabated, maybe the secret lies in the US Treasury, or like everyone else we are going to have to react to the next VAR Shock where and whenever that occurs.

It’s getting difficult to know which data point to trust these days and I am reminded of the 2011 movie and article title, whereby its near impossible to get to the bottom of what or who to trust. So lets play out the game.

TINKER - Central Bank Monetary Policy

As Jerome Powell reads at the beginning of every single FOMC Presser (and this weeks was no different on 26th July).

“Price stability is the responsibility of the Federal Reserve, without price stability, the economy doesn’t work for anyone. In particular without price stability, we will not have a sustained period of strong labor market conditions that benefit all.” - Fed Chairman, Jerome Powell.

It’s an interesting concept, as the Fed raised interest rates another 25bps to the range of 5.25%-5.50% Fed Funds Rate and US Headline CPI dropped from 4.1% to 3.0% YoY for the month of June 2023. At the same time, US GDP has been above 2.0% growth for the last 4 quarters and the Unemployment Rate has been range bound 3.4%-3.7% for the same period.

Even with the elevated levels of inflation / the price instability the Fed are trying to avoid, lets not forget that historically we have lived in a deflationary environment. Despite the price instability and ongoing rate of inflation, the US Economy has been strong in comparative GDP terms and the Labor Market is robust (again in comparative terms). So to surmise, what the F*#k! is Powell talking about? I’d proffer that price stability and a robust labor market may not go hand and glove any longer….

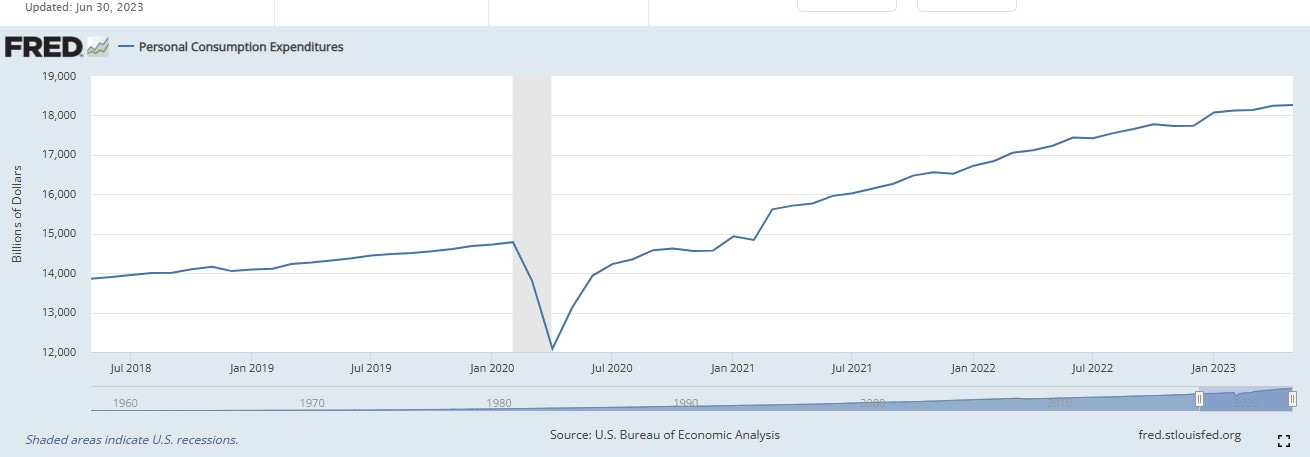

TAILOR - US Consumer Spending

For sure the narrative has been for the last number of months that the purchasing of products has reduced dramatically compared to the increase spend on services as people continue habits of eating and going out after 2 years of mandated lockdowns.

But the market betrays such a narrative, in particular when you consider the Dow Jones Transportation Average Index, i.e. the companies that move stuff. The DJTA has climbed from 13,780 in early May 2023 to what seem like overbought levels at 16,621 today, an increase of 20%+. Things are moving around the USA.

People haven’t stopped buying stuff, its just not at the same levels of 2020 and 2021, but as you see the number is going up and to the right in true NGU style.

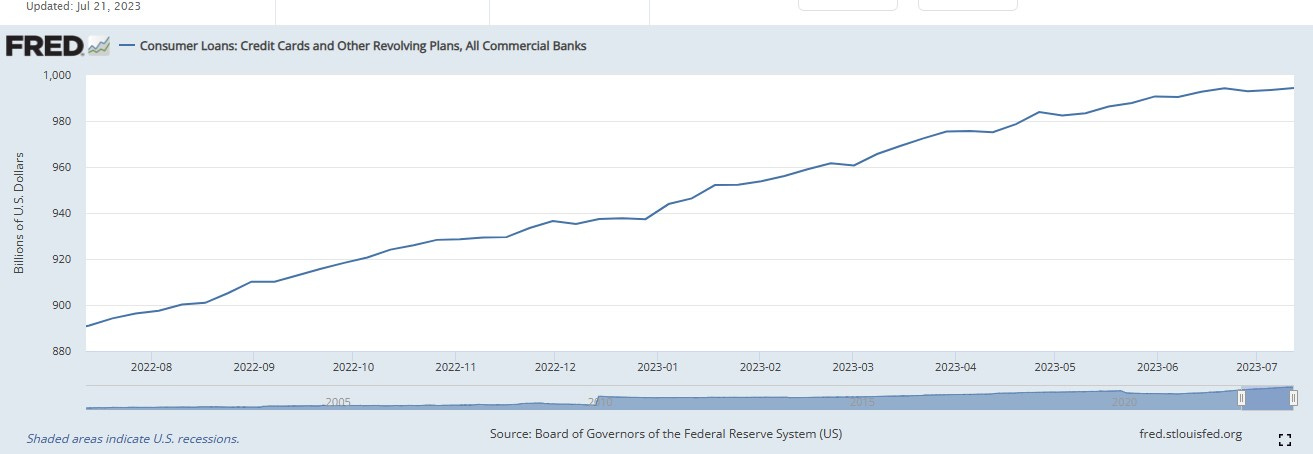

Revolving consumer credit card keeps moving in the same direction.

SOLDIER - J’accuse la Yield Curve

Ah the Inverted 2s/10s what a delightful pair you make, you’ve grown apart of late, but we always thought you would get back together. However, the months rolled on and on. Now like a loveless marriage they are like ships passing in the night, mirroring each others movements but they never do it together.

This inversion indicator of a recession in 12-24 months (March 2022) has been the worst or best known signal that the world and its mother have been clinging onto for nearly 18 months. But when will the yield curve invert and what form will the steepener occur? Will the front end fall (bull steepener) faster than the back end, or will the back end rise above the front end (bear steepener - as we have witnessed in the last 12 hours post BoJ YCC statements on their JGB10YR yield target).

The yield curve will correct, but we don’t know when, and we can only guess how. I did believe that it would initially come via a bull steepener, i.e. when the Fed cuts rates the front end would collapse under the back end, however recent events give me cause to pause and rethink this assumption at least for a couple of quarters.

SPY - ????

This is one that we won’t know until it happens. It will be headlined as the root cause of all problems, however it may only be a catalyst of something much bigger.

We had the Nickel Market nearly bankrupt the LME Clearing House, with trades having to be unwound. We had unfunded tax cuts from the UK in Oct 2022 nearly wipe out LDI and Pension Funds to boot. Lets not forget the US Bank Unrealized Losses caused by huge inflows of cash deposits used to buy out of the money long dated US Treasuries and MBS products. Credit Suisse (cough cough), or a War in Europe. I nearly left out the well signposted Commercial Real Estate crisis with WFH running a muck and causing Office Voids and Defaults.

BUT

What will the next thing be? I’m scratching my head still (I think there is a strong chance that it is insurance and reinsurance when Balance Sheets will be tested by some VAR Shock in the future). All I know is that when it does happen there will be lines of people queueing up on Twitter/X and Substack claiming that they saw it coming.

Conclusion

In any event, we all suspect someone or something and one thing is assured. All the aforementioned players will have contributed in some way to the next VAR shock. We can only manage risk in line with our own tolerance and timelines.

Best of luck out there and enjoy the rest of your summers.

Cheers

A Walking Gentleman.

I also deem it could be insurers, although many claims It cannot happen as they don't have to market to market. But so were many claiming for the (US) banks as well. Not sure...

What will the next thing be? I’m scratching my head still (I think there is a strong chance that it is insurance and reinsurance when Balance Sheets will be tested by some VAR Shock in the future). All I know is that when it does happen there will be lines of people queueing up on Twitter/X and Substack claiming that they saw it coming.