Who cares about the Past? Its about the Future

Who cares about the Past? Its about the Future

Time to make some 2024 predictions

Merry Christmas and Happy Holidays to all my subscribers (old and new). It has been a while since I had time to jot my thoughts down, so here goes.

As the late, great Yogi Berra (baseball player) once said “Its deja vu, all over again.” Another year is almost behind us and its time to reflect on the last 12 months and more importantly to look ahead to the next 12. With that in mind I will take a swing at a couple of pitches for 2024.

In everything that is considered below, please note that nothing goes up or down in a straight line and there are bound to be the usual ebbs and flows throughout the year. Please note the disclaimer at the end of the article and understand that I have a long time frame for investing, I am not a day trader and I avoid leverage wherever possible.

If you read my articles from last year, you will see that my investments sometime take months to pay off, but I am fortunate enough that a lot of my 2023 investments did pay off.

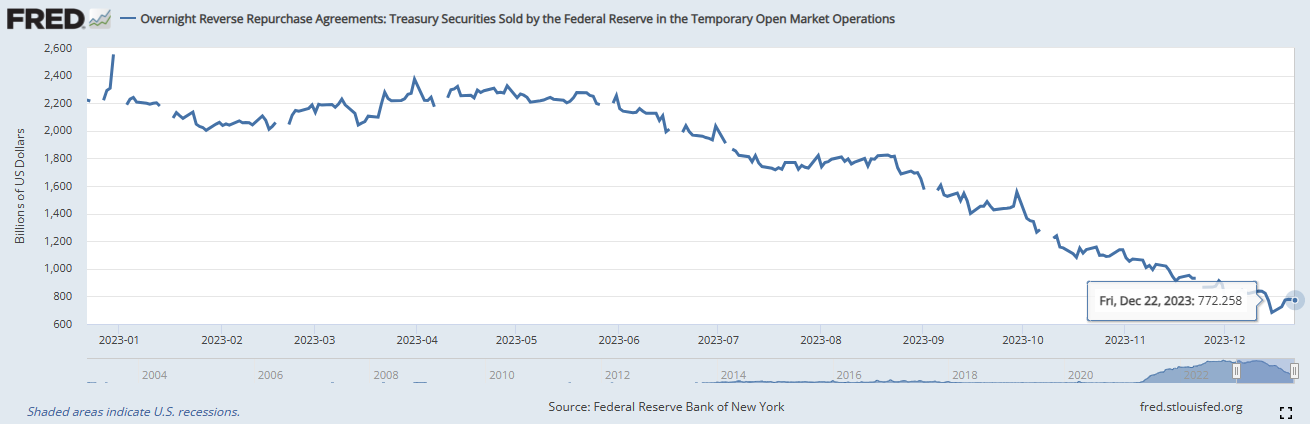

1 - Reverse Repo (“RRP”) Facility will be fully drained.

The RRP sits at $772 Billion, down from its FY2023 peak of $2.553 Trillion prior to the raising of the US Debt Ceiling in mid 2023. This downward trend will likely continue, particularly if US Fiscal debt is funded by shorter term T-Bills, which has been the case. It seems that the US Government doesn’t want to commit to longer term debt given the high yields at play. This will tie in to a later prediction on Bonds and overall liquidity.

2 - Equities will continue to rise - SPX to breach $5,500

I have written before, as the RRP drains, that there is more liquidity in the market from the collateral multiplier effect. This liquidity and debt refinancing will assist a loose set of financial conditions which will also be supported by ongoing US Fiscal Deficits. The weaker USD performance globally from his recent strength will help US Multiple-nationals earnings performance with foreign currency all of sudden being more valuable in their Income Statements.

In addition, we are in a Presidential Election year and it is very likely that the incumbents generate all sorts of stimulus and incentivizes to bolster their chances at the polls. This will further add fuel to the fire for “Risk On”.

SPX, for me, is forming a Large Cup and Handle Pattern that I have really heard spoken about, indicating that it is not a perfect pattern. The measured move price target is $5,733, so I will go in under with my prediction at $5,500 (taking profit before a blow off top so to speak). Expect a retest of support at the $4,600 before any fireworks at the neck of the handle possible breakout.

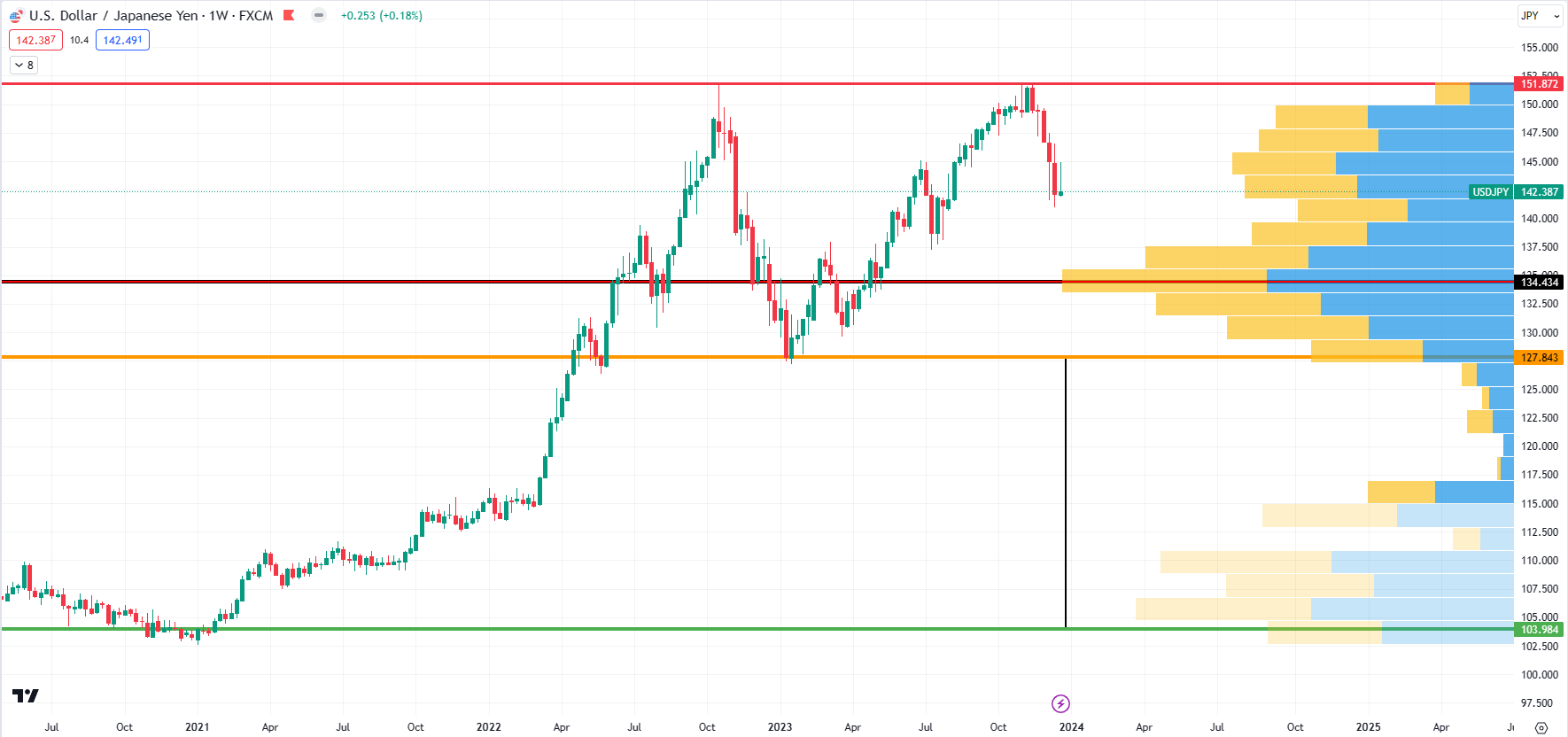

3 - Yen will outperform other Global leading currencies

The Yen has been the poor cousin compared to the Central Bank Family. The BoJ has indicated of late that it will begin to “normalize” interest rates, that means moving away from a negative interest rate environment - which is quite literally where they have been for decades, remaining in negative territory while their peer nations hiked interest rates, so much that they nearly killed their banking system.

The USD/JPY breached $150 for a good portion of Q4, only reverting to the low $140’s in December. Perhaps this momentum shift continues and we could see USD/JPY as low as $103 if both the $134 (black line) and $127 (orange line) levels are broken. There is a lot of trading volume historically at the $134 (point of control). If both are broken, the 200DMA (not shown) on the Weekly Chart sits at $122.54 with very little trading volume until $113-$115 and we could well wick down below $110 in a sell off of USD. A USD sell off and a possible $103 would only likely occur in the event of a severe Fed Funds Rate cutting cycle, in the absence of that it would be that the BoJ actually raise interest rates after decades of negative rates.

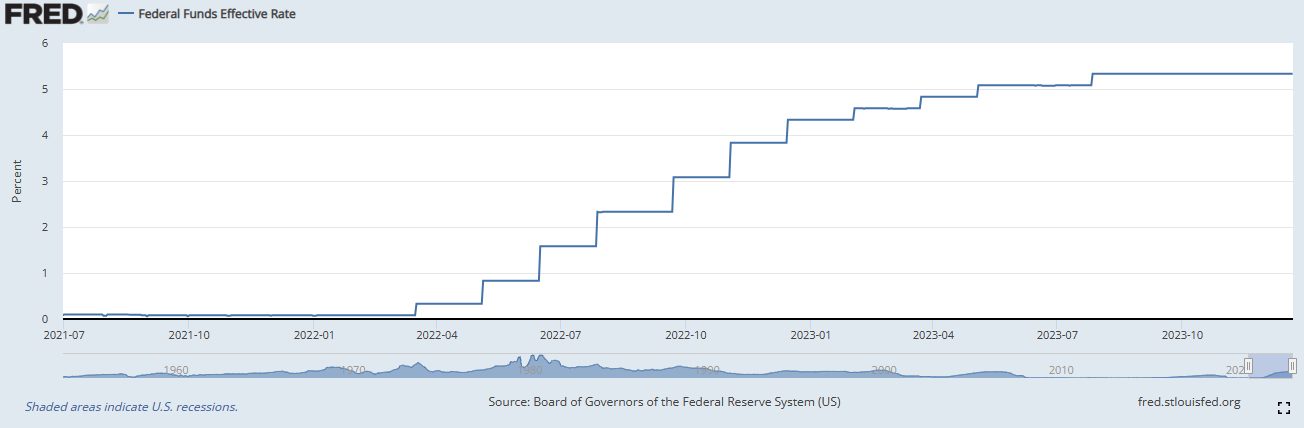

4 - The Federal Reserve will Cut Rates later than the Market Expects

The US is definitely in an era of higher for longer. Strong Unemployment data and positive US Nominal GDP (again supported by US Fiscal Spending leading to Deficits) will allow the Fed to maintain rates at 5.25% - 5.50% for longer than thought. For me, I try to keep it simple, you need factor in that the Fed is a lagging institution. They will never front run economic data and as such they will be late and they will over play their hands. There is no point in the Fed cutting rates by 25bps. When they cut it will be a deep cut and it will be reactive.

As I look at this chart and history, I can’t see a scenario whereby the Fed take the incremental steps down, for me it will more likely be “steps up, elevator down”. And I don’t see anyone pressing the elevator buttons just yet when you look at the US Unemployment Rate.

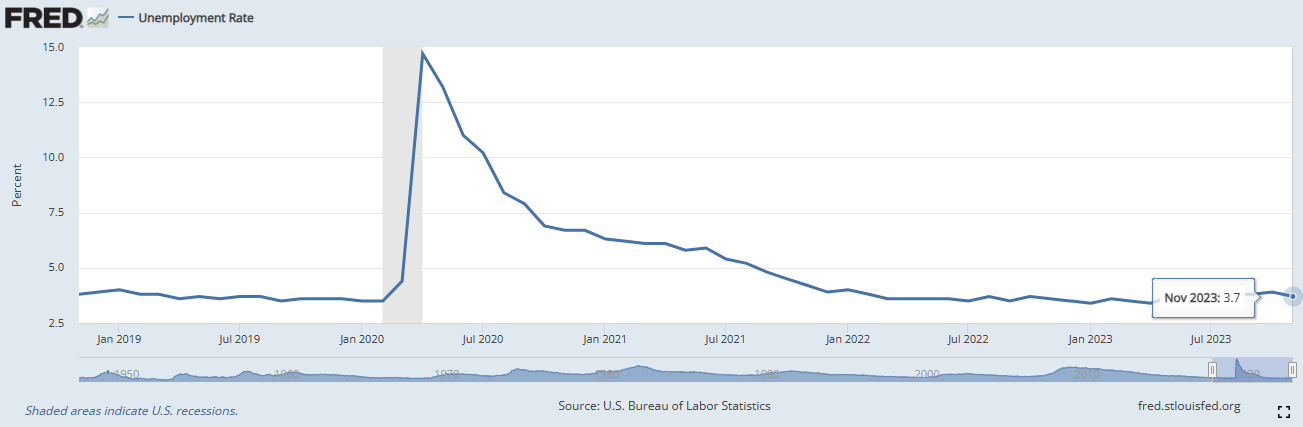

The highest Unemployment Rate that the US hit in FY2023 was in October at 3.9% and it closed the year (from a print perspective) at 3.7%. In my view and listening to a lot of FOMC pressers, the Fed is unlikely to cut rates unless these numbers hit above 4.4%.

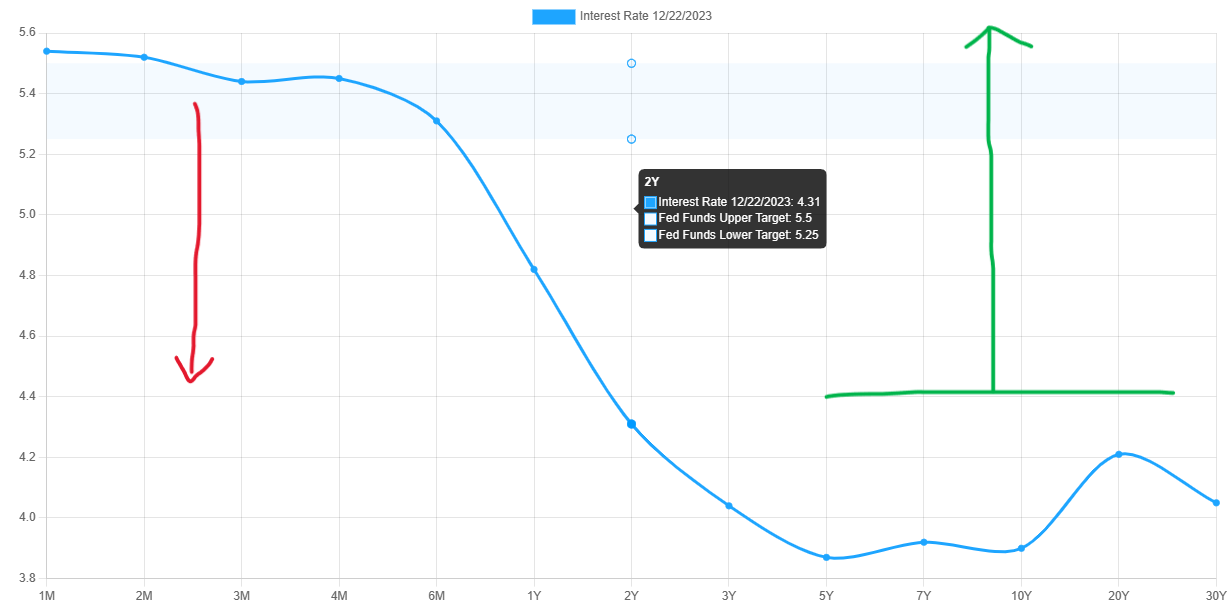

5 - While US Short End Bonds fall, the Long End Bonds will sell off

I wrote extensively on my Short TLT positioning throughout FY2023 and the logic remains in play. I see the US Yield Curve normalizing and with that if the Short End, say US02YR trades at 4.75% (I think this is likely for a while), then the Long End, say US20YR will trade with a 150bps duration premium, i.e. 6.25%. At 6.25% this would take TLT down to the mid $70 level. I have entered half of my target position for FY2024 already at BEP $98.28. I have not fully decided how to deploy the remaining 50% of the target position.

The Short End, T-Bills and Notes will catch bids as the US Fiscal Deficit borrowing will target short duration instruments to ensure that they aren’t paying huge interest bills in perpetuity and get caught in a debt cycle of borrowing to pay high interest payments (which they are doing in the short term).

The US Fiscal Debt will not be falling anytime soon.

6 - HIGH Beta Stocks will outcome Value Stocks

I’m going to measure this by the NASDAQ v SPX over FY2024, but in truth there is so much overlap with the 7 MEGA CAPS (or Magnificent Seven) that there will be little between them. However, the premise is that Discounted Cash Flows with modest growth will be less attractive than High Growth Stocks. This productivity in earnings will have been driven by a higher return demand on capital invested and will likely help to increase US GDP.

Above all else a weak USD will help fuel an equity rally and a higher or prolonged rate of inflation will also assist the growth of US Nominal GDP. This in turn will help combat high US Debt : GDP ratio which sat at 123% in Sept 2023, it will be a balancing act to bring this back to a 10 year average of c.105%.

My Conclusion

My over-riding take away is a weaker US Dollar internationally will give grounds for a “Risk On” environment and the Japanese currency will likely to lead the charge. Liquidity will ultimately dry up as the RRP drains leading to the question of who is going to buy all the US Treasuries needed to fund the US Fiscal Deficits a strong H1 2024. Either legislation changes to force Pension, Insurance Companies and Banks to leverage their US Treasury Holdings in order to buy more Treasuries or we see the Federal Reserve recommence Asset Purchasers in the latter part of the year, which would coincide with November’s Presidential Election. If anything the Regional Banking Crisis and the resultant Fed actions should give comfort that the Fed will continue to be the back stop.

No one can be 100% right all the time, these predictions statistically are bound to be wrong in one way or another, but my take is that the direct is correct and I want to be positioned for that, with all the necessary risk management protocols you’d expect.

I started with a Yogi Berra quote and I will end with one too.

“It's hard to make predictions, especially about the future.” - Yogi Berra

NB: This is not financial or investment advice and you should contact your own independent financial advisor before deploying any of your hard earned cash into these markets. Please do make your own risk.