US Deficit not about Interest Rates

US Deficit not about Interest Rates

CBO Projections highlight blended rates bottom out.

The CBO or the Congressional Budget Office produces updated US Fiscal Projections from annually but quite randomly. The most recent projections were released in February 2024 and prior to that we had been working off May 2023 numbers. There has been a lot of commentary that the increasing level of debt along with the higher borrowing costs (US Treasury Yields) will create huge deficits.

Well in these CBO projections, does the Rate of Interest (Treasury Yields) for the US Government made a dramatic difference to growing cumulative US Public Debt? In short, the answer is no, but lets dive into the actual numbers.

Remember, for me at least, the US Fiscal Deficit is the biggest directional indicator of a bullish market that I can see. In essence it is QE in disguise. The US Government continues to borrow its Deficit, creating New Dollars in the form of New US Treasuries. But as I mentioned, lets have a look at the actual numbers.

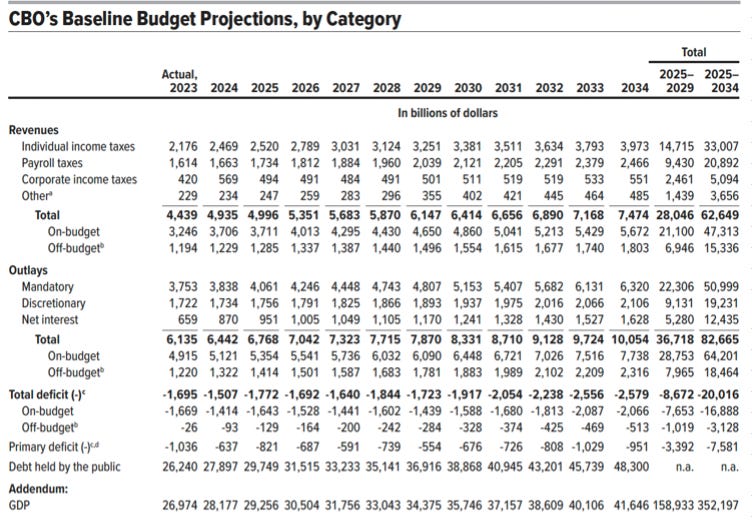

In the above table you can see the actual Deficit in 2023 sat at $1.695TN (yes that is trillion). Of that Deficit the interest bill accounted for $659BN (billion) / 38.87% of the Total Deficit. Yes it is clear that the Interest Liability grows Year on Year in line with the increasing Fiscal Debt.

So if we exclude Interest there was a whooping $1.0TN Fiscal Deficit which will have been funded by the issuance of new US Treasuries, but more realistically shorter term Debt in the form of Bills and Notes. In no way is the US Government selling huge amounts of 20YR and 30YR Debt at 4.5%, rather they are issuing short dated paper that make a small variation in their Blended Interest Rate.

We also see a sub 100% Debt:GDP in 2025 before continued Fiscal Running Deficits lead to 115% Debt:GDP by 2034 when the Public Debt is forecasted to be a monstrous $48.3TN (trillion).

So we actually see an average interest rate increase in 2023 to 2024 of 2.69% to 3.31%, which is a big enough jump (62 bps) but then projections of average interest rate soften from a rate of change perspective to 3.38% in 2025 dropping to 3.31% in 2028.

So we are seeing Interest Rates having a huge spike comparatively to existing US Treasury Yields, largely because the current US Debt has secured lower interest rates. Remember its the spending that causes the majority of the problems, the accumulating debt and not rising interest rates.

What does this all mean?

Well the US continue to spend on Mandatory and Discretionary expenditure in these projections (regardless of Republican and Democrat - I would imagine). This spend will drive the US Nominal GDP and create an inflationary cycle.

The Fed will have to stop its roll off of US Treasuries and begin Re-financing the existing Debt, perhaps even at preferential rates to mandate the average interest rate.

If the US Treasury is forced to issue new Debt, it is more likely to continue its current policy of selling short dated Bills and Notes, this means that there would be forced demand at the short end, driving this yield down, while the long end will become more scare and perhaps less in demand due to duration risk and its yield will push upwards which could create the environment for a normalising of the US Treasury Yield Curve (excluding the Fed Funds Rate / Overnight Rate).

How does this affect positioning?