Powell channeling Bob Marley

The Next FOMC is only 2 weeks away on 14th June and market participants are getting their knickers in a twist whether the Fed will 1/ Hike 25bps 2/ Pause or (more unlikely) 3/ Cut. It gets you thinking about the macro landscape when there is a broad consensus on some important data driven event. What has the Fed and its Chair, Jerome Powell been saying and will they walk the walk?

Powell (to me at least) has been channeling the legendary Jamaican musician, Bob Marley and his band, The Wailers. Here is why……….

Stir It Up

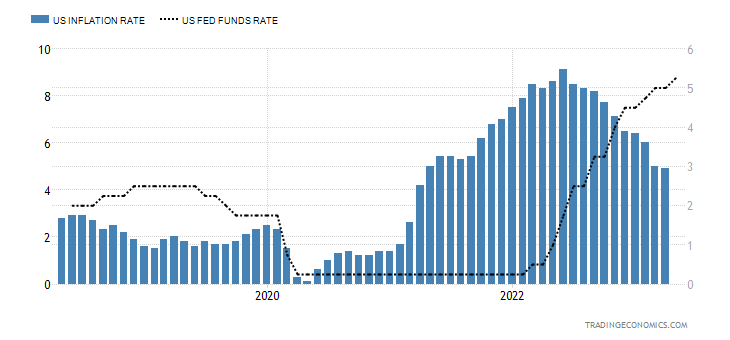

Into 2021 and the Fed FOMC narrative was that inflation was “Transitory” and a result of supply chain imbalances and that there was no need to hike interest rates to meet a growing CPI number. US Headline CPI had historically been around the Bernanke (former Fed Chair) invented 2.00% target, nearly falling negative in Q1 2020.

The Fed did not start to increase the Fed Funds Rate until March 2022 with its first 25bps hike but its easy to forget that US CPI was above 8.00% at that time and the delta was >7.50% between rates and inflation. The inaction of the Fed in raising interest rates helped lead to a spiraling of upward inflation which only started to decline YoY in summer 2022 but has remained uncomfortably sticky at 4.9% as I write. The pot had truly been Stirred Up.

Redemption Song

The Fed realized that it was behind the 8 Ball and began its hiking cycle which really kicked into gear with three consecutive rate 75bps rate hikes between August to November FOMC Meetings taking rates from 2.50% to 4.00%, before reducing the pace of hikes to 50bps then to 25bps at FOMC Meetings to the May 3rd FOMC Meeting with rates sitting at 5.25% as I write. Important to note the $95BN of Monthly QT of rolling off T-Bills and MBS Products, which was supposedly to reduce liquidity in the marketplace.

Powell had to stake his claim for redemption having lagged behind inflation for so long, he was going to have potentially break things in order to tame the beast.

Could You Be Loved

To this end will Powell be remembered as the Arthur Burns of the Fed Chair World or could he be loved in the History Books and marked down for Fed Chair Heaven like his boyhood idol, Paul Volcker. This is more about legacy than most people think.

Fed Chair Powell chose the latter and started the climb for rates to exceed the Headline CPI print to the destruction of 3 high profile US Regional Banks. Who cares about Bankers when Gasoline prices were falling. In particular the Fed wants to avoid having a double spike of inflationary impulses experienced historically.

Every Little Thing is Gonna be Alright (“Three Little Birds”)

Throughout Senate and Congressional hearings and in the now mundane commencement address at each FOMC presser, the Fed is focused on its’ dual mandate of Price Stability and Employment. Repeatedly we have heard that the Labor Market is tight, Unemployment has ranged from 3.4% to 3.7% over the last 12 months. Jobless Claims have consistently been lower than forecasts and the JOLTS number (Job Openings) while reduced recently still represents over 1.5 available jobs to job seekers.

Everything will be alright, ok we have gone from a Soft Landing narrative to a Softish Landing narrative to a Mild Landing narrative. What we have seen is that the Fed are willing to break some things and act swiftly to create stop gaps with not everyone is safe. Bank Equity and Bond holders were not bailed out via Signature Bank, SVB or First Republic.

Conclusion

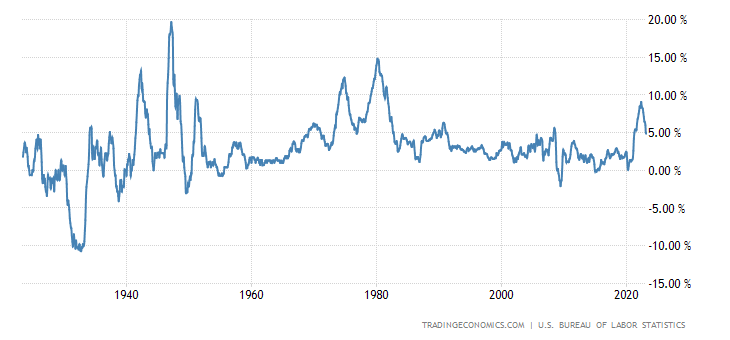

Bringing the articles premise all the way home we are set for rates to be “higher for longer”. The Fed doesn’t want to experience any double spike in inflationary impulses like in the historic post WW2 and 1980 eras. There are data sets that support a stronger economy via the Unemployment Rate (one of the two mandates of the Fed) so Price Stability is the pure focus in Chair Powell’s eyes.

With the recent Core PCE and Headline CPI proving that Inflation is indeed sticky and could potentially tick back upwards, we may in fact see a final rate hike of 25bps (who knows) taking us to 5.50% but what I am certain of is that Interest Rates will more than likely stay higher for longer, its just what the Fed are smoking.

My Positioning

Long Gold / Short Long T-Bills still looks like the trade. With the Fed interventions of the BTFP (“not not QE”), I’m still partial to High Beta over Value Stocks which rely on discounted cashflows. Please note I have no leverage on any positions and can withstand a drawdown if markets go against me. I do hold back some dry powder too (about 10%) to catch any dips.

NB: This is not financial advice and you should contact your own independent advisor before deploying any of your hard earned capital into this volatile markets.

Great analysis 👍

Great post, really insightful and a fun read