Macro Binoculars On - August 2023

Macro Binoculars On - August 2023

Where the hell are we?

I last wrote a Macro Review on Substack back in May 2023. Macro moves like a snail and my investment strategy is very similar, little or no movement. Perhaps though its time to pay attention and look through the wider lens again. With that in mind, I’m picking up the dagger and having a stab at the already bloody macro landscape. Its probably worth noting that I have curbed back on my 3rd party research and financial podcasts, so this will be my own unfiltered viewpoint.

Remember this is a free subscription and if you want to support me you could consider using my Virtual Data Room product, Dillie (if applicable to your business) at www.dilliedr.com or join the Dillie Substack at https://dillie.substack.com/

Please drop a like or a comment as it really helps to drive my free subs or buy me a coffee via the link here https://www.buymeacoffee.com/walkinggentleman

The Baseline Premise - Higher for Longer

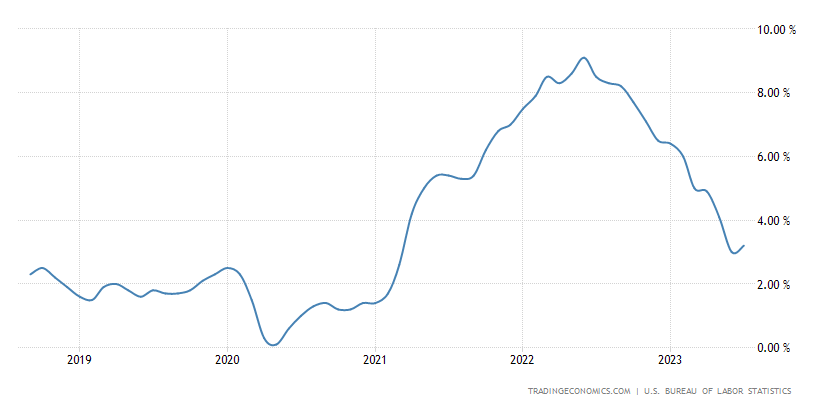

Powell has been consistent in his approach this year (and last) and has continued hiking rates with the exception of one pause or skip. The mantra or narrative is very much we are staying higher for longer. Looking at the August CPI print this does make sense if indeed the arbitrary 2.00% inflation target is the Fed’s and the ECB’s goal (as opposed to a measure). CPI bounced up from 3.00% to 3.20% YoY but was trending at 0.2% MoM so while the YoY has crept up the trend (granted) is downward. Downward but not at 2.00%.

The next CPI print (for August) is due Wednesday 13th September. My expectation is that it will creep slightly higher, only for the reason that the descent was so aggressive from the peak 9.1% in June 2022 that statistically data will stabilize when you look at a YoY basis. The fact remains that prices are still high, they haven’t dropped. While we have experienced disinflation, we are not in the deflationary environment we have come to hold so dearly.

As CPI stabilizes at 3.0% or increases slightly, the Fed will remain consistent leaving the Fed Funds Rate at 5.25% - 5.50%. While another 25 bps hike might still be possible, we are coming to the end of the hiking cycle in the US at least, the ECB might have further to go.

Second Thesis - The Rate Cut / The Bull Steepener

In addition to the higher for longer monetary policy view point, I’ve a lot of conviction in that a recession will emerge, but will only be truly signaled (perhaps a lagging signal) when the Fed cuts interest rates. In essence, I want to be out of the market just before there is a rate cut as this will (for me at least) trigger a monster sell off.

So, when will the Fed cut interest rates? There have historically been three measures for calling an imminent recession and they are

ISM PMI Manufacturing Index gets below 50 (occurred already this cycle)

An Inverted Yield Curve (the 2s'/10s have been inverted since Mar 2022)

An Interest Rate Cut. (we will delve into that now.)

The market is pricing in 5.5% Fed Funds Rate between now and the Year End, as shown above, but indeed the 3 Month SOFR Futures remain in the 94.5’s range until March 2024. This would indicate that the market is anticipating a 25 bps rate cut in by the end of Q1 FY2024 with SOFR Futures rising to 94.73

Furthermore the market is pricing in quarterly 25 bps rate cuts for Q2, Q3 and a 50 bps rate for Q4. This obviously doesn’t have to play out as “the market” anticipates, but it does provide an interesting indication of the potential macro future/monetary policy.

SOFR Futures (formerly Eurodollar Futures) purely indicate the front or short end of the curve, the Fed Business End. The long end of the curve (the longer duration bonds) as mentioned above have been inverted for a year and a half. How this inversion is reversed will be pivotal to the severity of the recession. A bull steepener is when there is a rate cut at the front end, driving SOFR closer to 100, and the front end down faster than the long end.

Currently without the Rate Cut, we are starting to see signs of a bear steepener whereby there is slower decline or no decline at the front end, while the long end increases at a faster pace. With the Fed’s higher for longer strategy it looks like we will see this bear steepener play out a little while longer too.

The front end is basically flat within the current Fed Funds Rate 5.25% - 5.50% and moving in small daily percentages.

While the long end (beyond the 2Year) is pushing out and moving in much bigger swings at 1.35%+ daily percentage (not yield) moves.

Positive US GDP

Another factor aside from Inflation for Bonds is the GDP rate. If CPI is 3.2% YoY and the Annual Growth Rate of GDP is 2.6%, you could add those numbers together to get 5.8% and come relatively close to the Long End / Long Duration terminal rate/yield, i.e. the 20YR hitting the 5.8% range, this would likely reverse the inverted yield curve via the bear steepener and could be supportive of a “soft” / no landing for the US Economy.

The more I look at the US economy and consider the higher for longer strategy, the more I think we could well be in a midpoint of a new business cycle post 2020. I mean that 2020 - 2026 being a full business cycle (7 years) and we are sitting in the middle likely looking at a mid cycle dip but realistically the cycle completes in 2026 with a heavy recession. Do I sound crazy? Then I probably am. But looking at the uptrend in US GDP it does look like a possibility at least.

The QoQ was 2.1% from the August print for July and the next print is due 28th September 2023. However, the Annual GDP Growth Rate at 2.6% and the obvious uptrend does suggest that we are far away from a recession compared to the end of 2022 when the Rate was sub 1.0%.

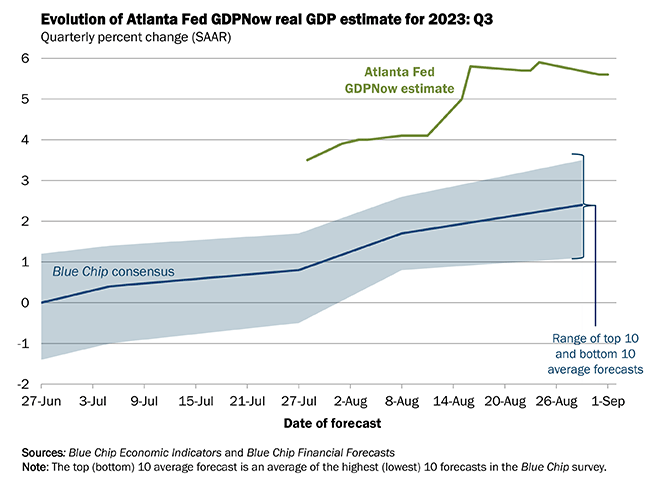

There is certainly bullish sentiment when you factor in the above Atlanta Fed GDPNowcast of the rolling QoQ growth in GDP, which they calculate at 5.6% for Q3 FY2023.

National Financial Conditions Index (NFCI)

The Chicago Fed issue the weekly NFCI and the latest print was 25th August. There should be another print coming shortly. The Index is at -0.40 and its important to mention that the tighter the financial conditions the closer you would be to 0 and a positive number.

The Fed was charged with tightening Financial Conditions in attempt to reign in inflation, however we went from 25bps Interest Rates and 4600 on the SPX to 550bps and 4600 on the SPX in just under two years so the QT and Interest Rate hikes haven’t really moved the dial for risk assets.

Indeed when you look at where we are comparatively at -0.40, the last time we were at this level was July 10th, 2020 when the SPX was 3,200 and broke higher from that week onwards. The question is, what level of financial tightening can the Fed execute now? They can’t raise rates much higher at 5.50% or they are further cripple the serviceability of US Fiscal Debt which is running at a massive deficit.

This just looks like a pivotal moment, whereby risk assets and the financial conditions that drive their price could go either way. But, it would likely have to be a heavy recession to tighten credit terms or some form of heavy banking failure that drives it. Any systemic failures have historically been bailed out and I can’t help but feel there is more room to the upside, despite this being, what I consider a contrary view and many market participants have a bearish or mean revisionist view.

US Unemployment Rate

The Fed has a dual mandate, price stability and full employment (or near full at least). The uptick in the most recent print does show signs of weakening from 3.5% to 3.8% but these unemployment statistics have been volatile enough over the last 2 years, ranging from 3.5% to 3.7%. While this could mark a breakout of that range we won’t know until the first week of October whether September data reflects this trend.

If we do see Unemployment break above 4.00% it could act as a trigger for the Fed to have a prolonged Rate pause and consider cutting rates. If there is a consideration of rate cuts, I see that being bullish for equities and store of value but when the rate cuts do actually come, as mentioned before I see that as a good opportunity to be risk off.

Conclusion

I certainly don’t have a crystal ball and there are conflicting data points at the moment. We have positive US GDP annual and quarterly growth estimates against a disinflationary backdrop. We have relatively loose financial conditions at -0.40 which was last seen in July 2020. Unemployment does appear to be ticking up but we are coming into an election year and I can’t help but feel the Biden Administration is placing a big emphasis on their Employment Numbers, so these could be protected to meet a political agenda.

While the market has priced in a rate cut by March 2024, I am having trouble reconciling that

On the face of it I remain cautiously bullish using no leverage and remaining long in my positions. Yes, there can be pull backs and we may see one in September, but I can’t see a Fed Rate Cut until 2024. The ECB will however continue to hike in my view, which will strengthen the Euro against the USD, potentially providing for a risk on environment over Q4. A weaker USD means stronger earnings for US multinationals for that period and the market will stay ahead of that curve (usually 6 months). Conversely a stronger USD would mean a weaker position for risk assets. I might do a follow piece on USD or DXY, but I think I’ve covered quite a bit already in this article.

Thanks for reading, please press the like button as it helps me a lot.

NB: This is not financial advice and you should consult your own independent financial advisor before putting any of your capital into this volatile market.

May I ask what was the reason you curbed?

Its probably worth noting that I have curbed back on my 3rd party research and financial podcasts, so this will be my own unfiltered viewpoint.

The tech industry is expected to continue to grow in the coming years, which will likely lead to even lower unemployment rates for tech sales professionals, hovering around 2%.