Is JPMorgan the JPMorgan of the US Banking Sector?

Is JPMorgan the JPMorgan of the US Banking Sector?

Expecting more uncertainty for US Regional Banks post 25bps+ FOMC

Over last weekend JP Morgan acquired the assets of First Republic Credit excluding any legacy issues. Any losses on the Loan Book would be shared with the State Body, FDIC. It pocketed a profit of $2.8bn on paper in the acquisition and this was the best offer for the Bank. It took on the Loan Book of $173bn of largely Residential Mortgages and $30bn of Securities, while also taking on the Deposit Liabilities of $92bn including the $30bn from 11 banks which we will repaid as part of the transaction. In essence, JPM, who have an abundance of deposits from the SVB and Signature Bank debacles now have acquired Assets (in the form of loans and securities) to balance it’s ledger.

Wall Street Journal LINK - JPM takes over FRC (details)

FRC was taken over by FDIC but was auctioned off before the actual seizure of the Bank. This sets a dangerous precedent in my eyes, whereby decisions get made but with the protection of the US Government behind them.

Now that FRC has gone under the JPM wing and post the epically bizarre or “broadly improved” FOMC presser by Fed Chair Jay Powell. We are now facing the next US Regional Banking run but actually this time there are a couple of candidates.

Powell’s performance at the FOMC presser appeared rattled and unconvincing when it came to the Banking Crisis which has been caused by huge USD creation backed up with a hiking cycle that today takes us from 0.00% (March 2022) to 5.25% (May 2023).

PacWest Corp dropped 58%+ in after hours trading on the tail of the rate hike and persistent commentary about higher for longer. News reports are confirmed that they are now in the auctioning progress and most likely liaising with the FDIC.

Western Alliance was down 30.00% after hours, perhaps not as deep as PacWest but nearly 1/3 of its Market Capitalization (CET1 Requirement) has been wiped in 90 minutes after the close.

The last specific bank to mention is Metropolitan Bank Holdings which was down 20%+ after hours. Again not as deep as the aforementioned banks, but it is more likely in the coming days and weeks that they could well be the next domino to fall.

The trick is that JPM are most likely tapped out now when it comes to US Regional Bank purchases as they now hold 10%+ of all US Deposits and they have to get special exceptional approval for the FRC deal.

Creating Competitive Tension

The FDIC’s board member McKernan reportedly states that the FDIC are widening the bidding pool for Regional Bank Assets to Non-Banks in order to get competitive tension and secure better prices are achieved.

Bloomberg Report Link - FDIC's McKernan and Bank Bidders

The main takeaway here is that they are expecting more Bank Auction or “Strategic Asset Sales” in the near future and within a half day it could well be the case. In the next case with JPM probably ruled out, it will be an opportunity for PNC to capture back some market share comparatively speaking to JPM or perhaps we seek Hedge Funds, Insurance and Pension Funds seeking to enter the Banking sector.

Bank Term Funding Program

With a balance of $81Bn declared as of 26th April (somewhat lagging), it appears that the “tools” that the Fed has to assist the “banking crisis” are not effective, nor that of the Discount Window. Banks don’t seem to be able to post collateral to redeem liquid cash to repay/honor depositors withdrawals.

There has been discussion now to increase officially the FDIC deposit insured limit from the $250k per account to a much higher corporate amount. This should assist but when there is a bank run, it is impossible to stop. The next step banking crisis playbook will be a ban on Bank Stock Short Selling which will quickly extend to all Financial Services Stocks (Insurance and maybe even REITS).

Conclusion

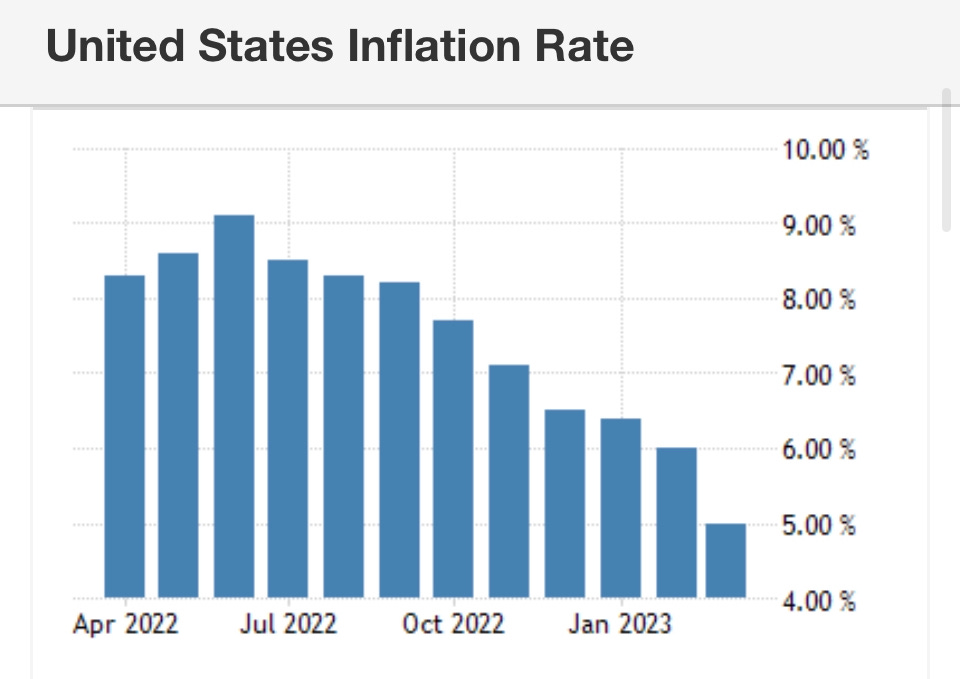

Its becoming more obvious that the Fed have hiked too far too fast. In particular as we have seen US CPI rolling over on a YoY basis from peak 9.1% to 5.00% in March 2023.

The three consecutive Fed rate hikes in 2022 at FOMC of 75bps each put stress on Banks that had bought US Treasuries to collateralize their huge inflows of USD deposits from newly cashed up Corporates and Individuals (remember 2020 when all those new dollars magically appeared). These unrealized losses and bank runs don’t seem to be protected by the Federal Reserves’ “tools” of the Discount Window or the BTFP.

I think we are only scratching the surface in banking terms, but in truth the 2008 GFC and aftermath destroyed a lot of small community $1Bn Banks which were either liquidated or absorbed into larger banks. FDIC increasing their insured limits looks likely to try and bring confidence back to depositors and a ban on Short Selling Financial Services Stock might help to ease for a while.

However the consolidation of the US Banking Sector looks set to continue but instead of the $1Bn smaller Banks of the past, we are left with medium to large sized $100bn Banks that are not as easily digested.

Thanks for reading A Walking Gentleman and be careful out there, its a bit gusty outside.